The Road to Understanding Retroactive Coverage Part 3: Retroactive Coverage

Last Updated November 9, 2023

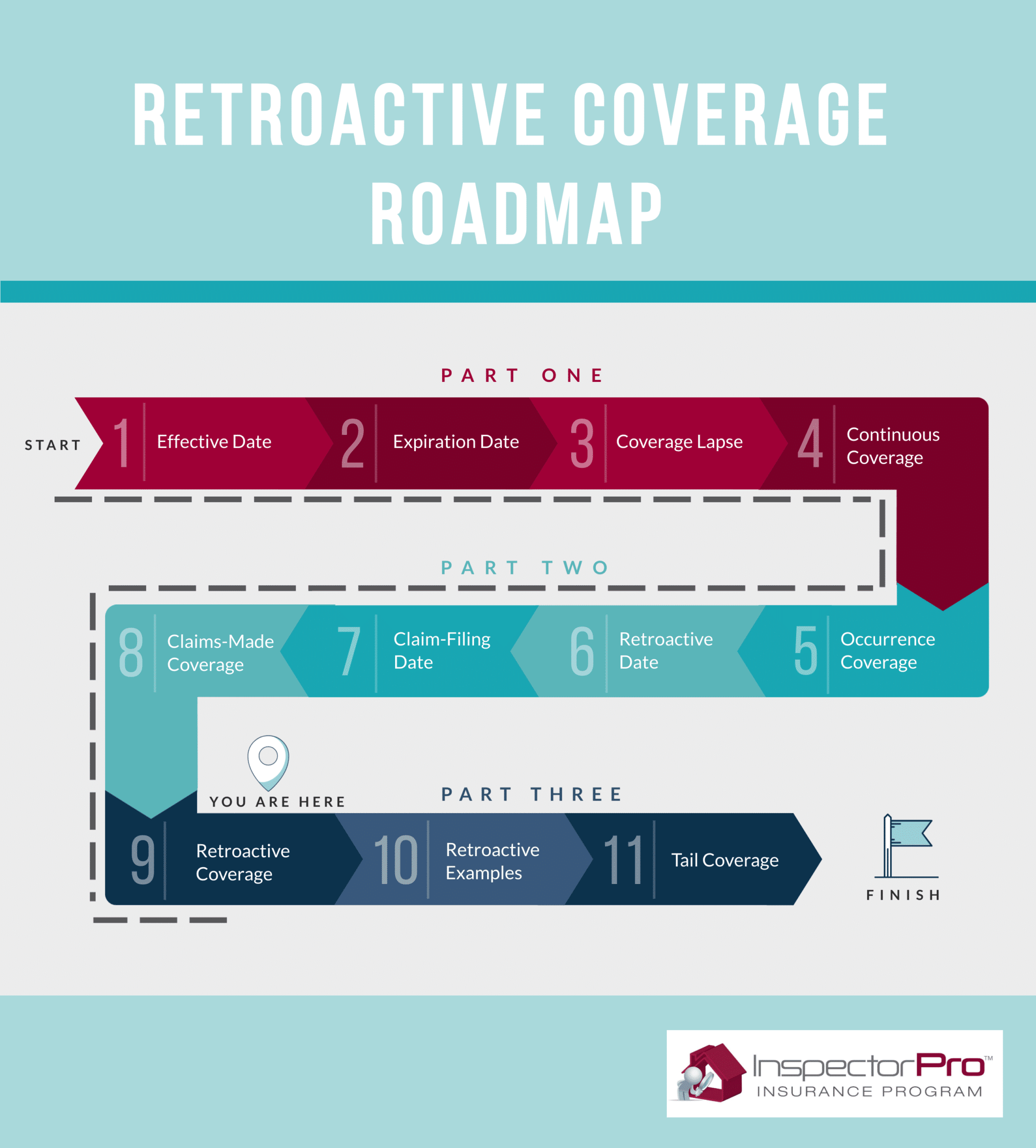

We’ve covered both continuous coverage and claims-made coverage, the two requirements to be eligible for retroactive home inspection coverage. Now that we appreciate these two terms and their own basic components, we can go into the homestretch of understanding retro coverage with confidence. See our roadmap below for reference.

So, retroactive coverage— What is it? How does it affect you? And how can you qualify for it?

We address these questions in the final installment of our article series below.

Retroactive Home Inspection Coverage

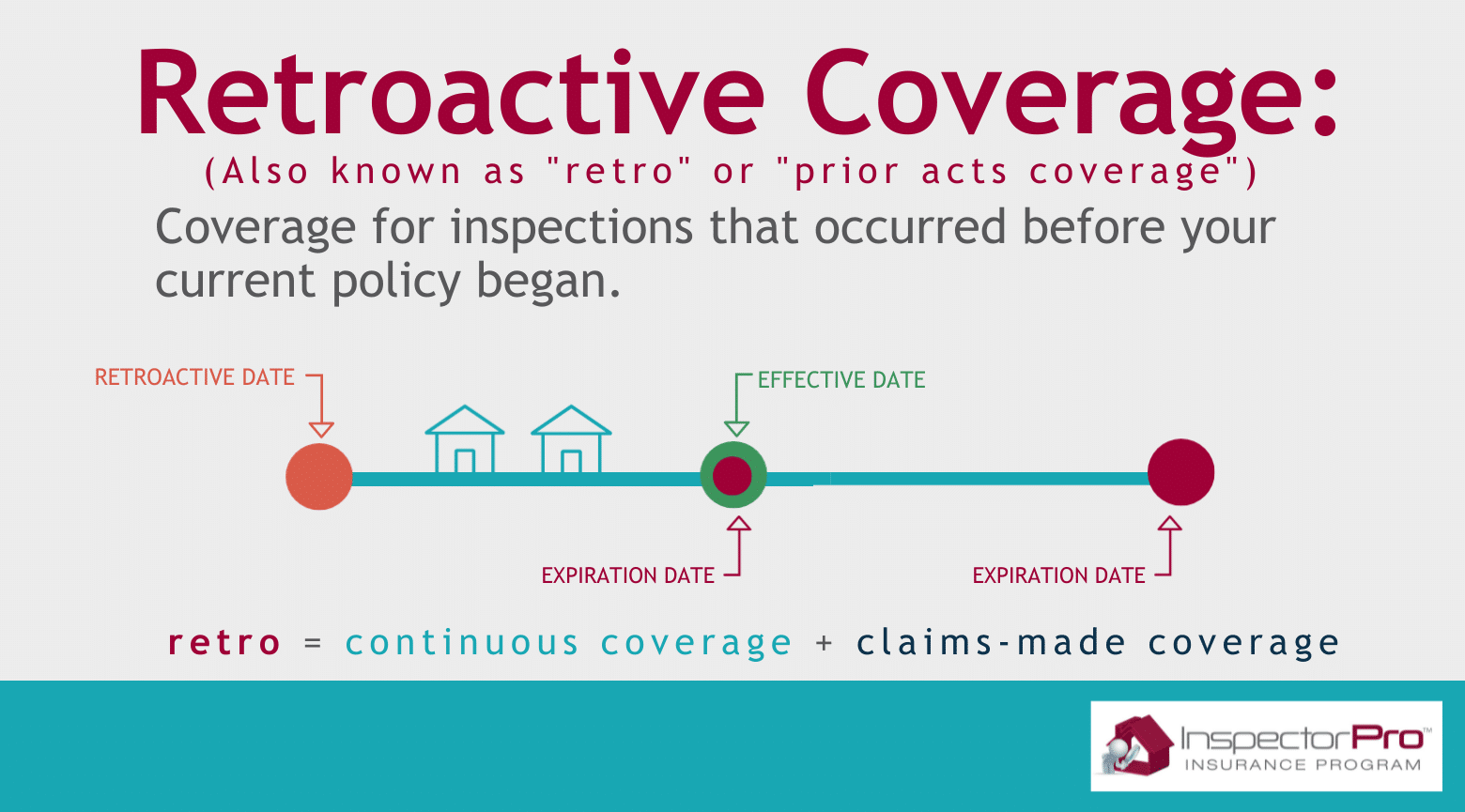

Retroactive coverage, also known as “retro” or “prior acts coverage,” gives you protection for inspections and associated claims before your current policy began. This can even apply if you were with a different provider (and if they chose to honor your retro coverage). But, in most cases, in order to qualify for retro, you must have a current claims-made policy and maintain continuous coverage.

Upon renewing with your insurance provider on time, you keep your retroactive coverage (should you qualify). If you switch to a new insurance provider, you must bind your new claims-made policy before your current policy expires. To do this, you must provide proof of retro coverage by submitting a copy of your former policy’s Declarations, in addition to completing an application.

The reason retroactive home inspection coverage is so important is because if you neglect to maintain it, you lose all coverage for inspections you performed before your current policy. For example, if you switch to an insurance provider that offers retro, you can’t apply the coverage to previous inspections and have lapse in coverage. Therefore, if a claim arises from a past inspection, your previous and current insurance provider won’t be able to protect you.

Beware of Policies Without Retro

Sometimes, insurance providers offer policies without retroactive coverage to drive down premium prices. Especially if you are a new inspector, it may be tempting to get quotes from these types of providers, and even bind with them. However, once you buy a cheap policy without retro, you can never get your retroactive coverage back. You can eventually switch to an insurance provider that offers retro, but since you didn’t maintain your prior acts coverage, you won’t have protection for claims that surface from inspections you performed while with your previous provider.

To illustrate the importance of having a policy with retro, let’s examine an actual claim filed against one of our insureds.

Retroactive Coverage Example

Example 1: Losing Retro

Recently, a former insured decided to come back to us. He’d gone with a less expensive policy that appeared to have similar coverage but, after a poor claims handling experience, he was ready to pay more for our better service.

Unfortunately, the other provider had sold him a policy without retroactive coverage. Switching to them had caused this inspector to lose 10 years of past inspection protection. And there was no way to get it back.

While he was disappointed to learn that he’d lost so much coverage, he was relieved to start a new policy—with a new retro date—with us and without the fear of going without prior acts coverage again.

Key Takeaways

The key elements we can take away from this example are:

- Don’t make coverage decisions just based on price. Look for quality insurance with extensive protection.

- Policies without retro cause you to lose coverage for past inspections.

- When switching insurance, look for a provider and policy that offer retroactive coverage.

- Verify that your retroactive date is correct when you receive your new policy on the declarations page.

Keeping these precautions in mind, what does it look like when you keep retroactive coverage?

Example 2: Maintaining Retro

Unhappy with the service his insurance provider was giving, a home inspector decided to insure with us. By providing proof of his retroactive coverage, and by avoiding a lapse, the inspector maintained continuous coverage during the switch.

Then, almost two years after the initial inspection, the inspector received a letter from an attorney representing a former client. The letter alleged that the inspector, realtor, and seller intentionally concealed water leaks, and that the new buyer had spent tens of thousands to repair the property. He demanded nearly $100,000.

After the inspector reported the incident, our claims team quickly sent out a letter of deniability, citing the inspection agreement’s limitation of liability clause. It took an additional two years of back and forth, but the claim was eventually dropped with no payout to the claimants and for the cost of the inspector’s deductible.

Key Takeaways

The inspection in question took place when the inspector was with a previous provider. But we were still able to defend him for the following reasons:

- The inspector had maintained continuous retroactive coverage with his previous insurance provider.

- The former policy was claims-made and offered retro, so we could pick up the coverage and defend inspections that were performed under the former policy.

- We had proof of the insured’s retroactive coverage because the inspector submitted the Declarations from his past policy.

- The inspector maintained continuous coverage by binding with us before the previous policy expired.

Because the inspector had taken these measures, we were able to cover and defend them.

Tail Coverage

The claim we just reviewed played out while the inspector was still inspecting. So how can you safeguard yourself from claims after you’ve stopped inspecting?

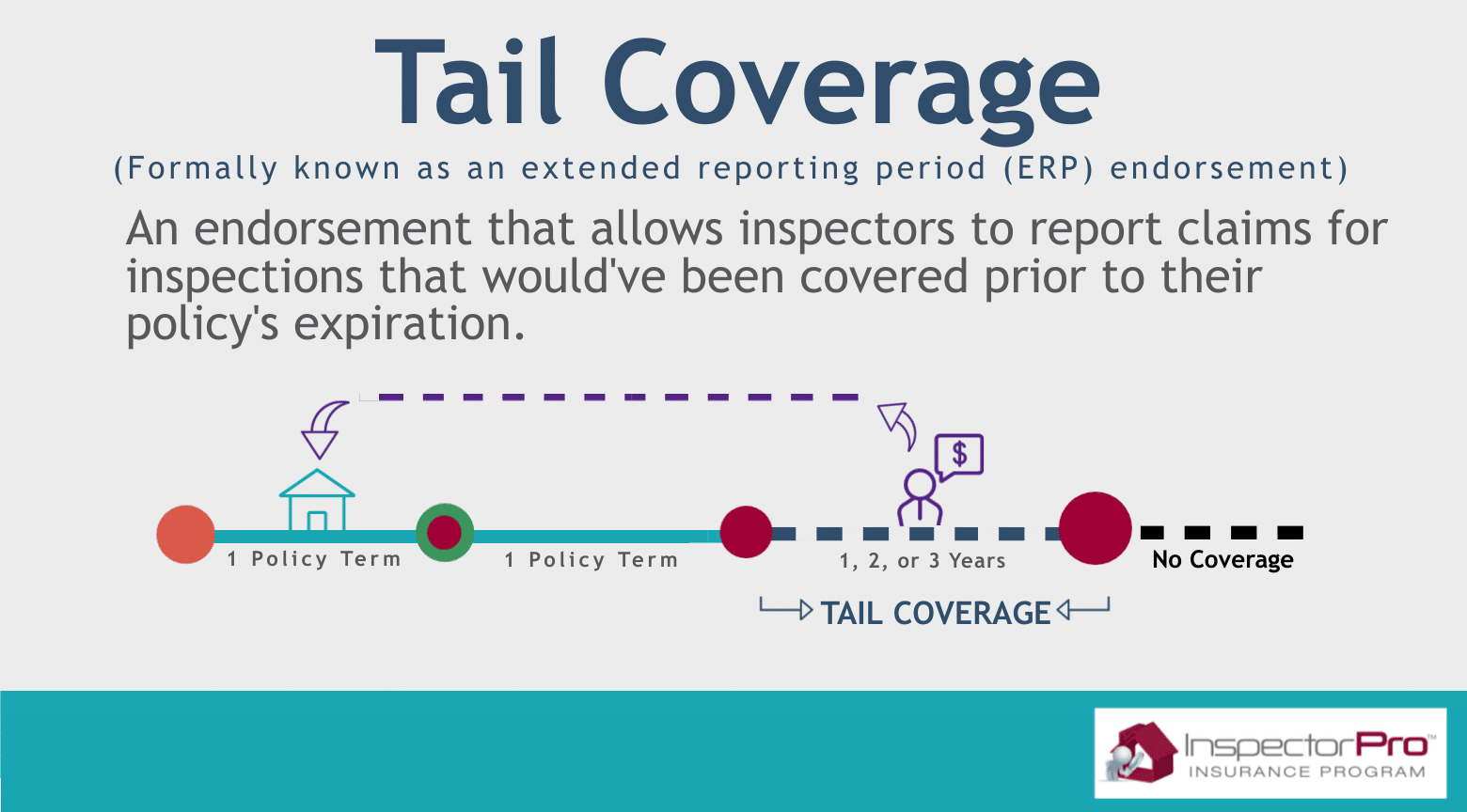

An extended reporting period (ERP) endorsement, otherwise known as “tail” coverage, gives you protection from claims after you have stopped inspecting. It allows inspectors to report claims for inspection that would have been covered prior to their last policy’s expiration or them leaving the business.

When a home inspector decides to leave the industry, their business, or their franchise, they should inform their insurance provider. From there, it is highly recommended that inspectors purchase extended reporting period endorsements in lieu of their insurance renewal.

If the policy is still in effect, the insurance provider may cancel the policy and have the tail endorsement begin on that same cancellation date. And, should the policy lapse at renewal, the inspector may still have time after the policy expires to purchase tail. Review your policy or ask your insurance broker for their tail purchase deadline.

Purchasing Tail

When purchasing home inspector tail coverage, you often have options. Typically, ERP endorsements come in one, two, or three years of coverage. Which option to purchase depends on your individual risk tolerance. (To learn about risk tolerance, see the conclusion of our article on insurance limits here.) However, there are a few things to consider when making your decision:

- Once you’ve bought tail, you can’t extend the coverage. For example, if you buy one year of tail, you can’t buy a second year at the end of that term.

- Whatever option you decide often has to be paid in full.

- Some home inspection franchises have minimum tail coverage requirements. If you’re a franchise owner, be sure to check to make sure you fulfill franchise tail coverage requirements.

Once your policy expires and your tail coverage goes into effect, you cannot perform additional inspections and receive coverage under that same expired policy. If you receive claims during your endorsement period, you will report them to your insurance company as you would normally. Once your tail coverage expires, so does your home inspection insurance protection.

Retroactive Series Conclusion

We’ve finally made it to the end of the road to understanding retroactive coverage. This concept is fairly complex. However, by breaking it down, we can grasp the significance of this coverage and how it functions. Given retro’s important, double-check with your insurance to see if your policy offers prior acts coverage.

If you do have retroactive home inspection coverage, make sure you renew your policy on time and pay your premium on time. Or, if changing providers, bind with them before your current policy expires. Then, check your new policy’s declarations page for your correct retro date.

If you don’t have retroactive coverage, choose an insurance provider that offers prior acts coverage. Moreover, pick a provider that makes obtaining and maintaining retro as painless as possible. After all, you and your business deserve the best protection.

InspectorPro offers claims-made policies with retroactive coverage. Find out about our program here. Apply for a quote here.